Choosing between a management contract and a franchise deal is becoming a core decision for hotel investors in Saudi Arabia. The pipeline is large. Saudi Arabia is set to deliver 358,000 new hotel rooms to meet rising tourism demand and prepare for major upcoming global events. At the same time, leaders at FHS Saudi Arabia say deal structures are shifting toward asset-light, flexible agreements, including lighter management contracts, performance-linked fees, and selective franchising. This is the context for evaluating a hotel management contract saudi arabia investors can live with over a long hold period.

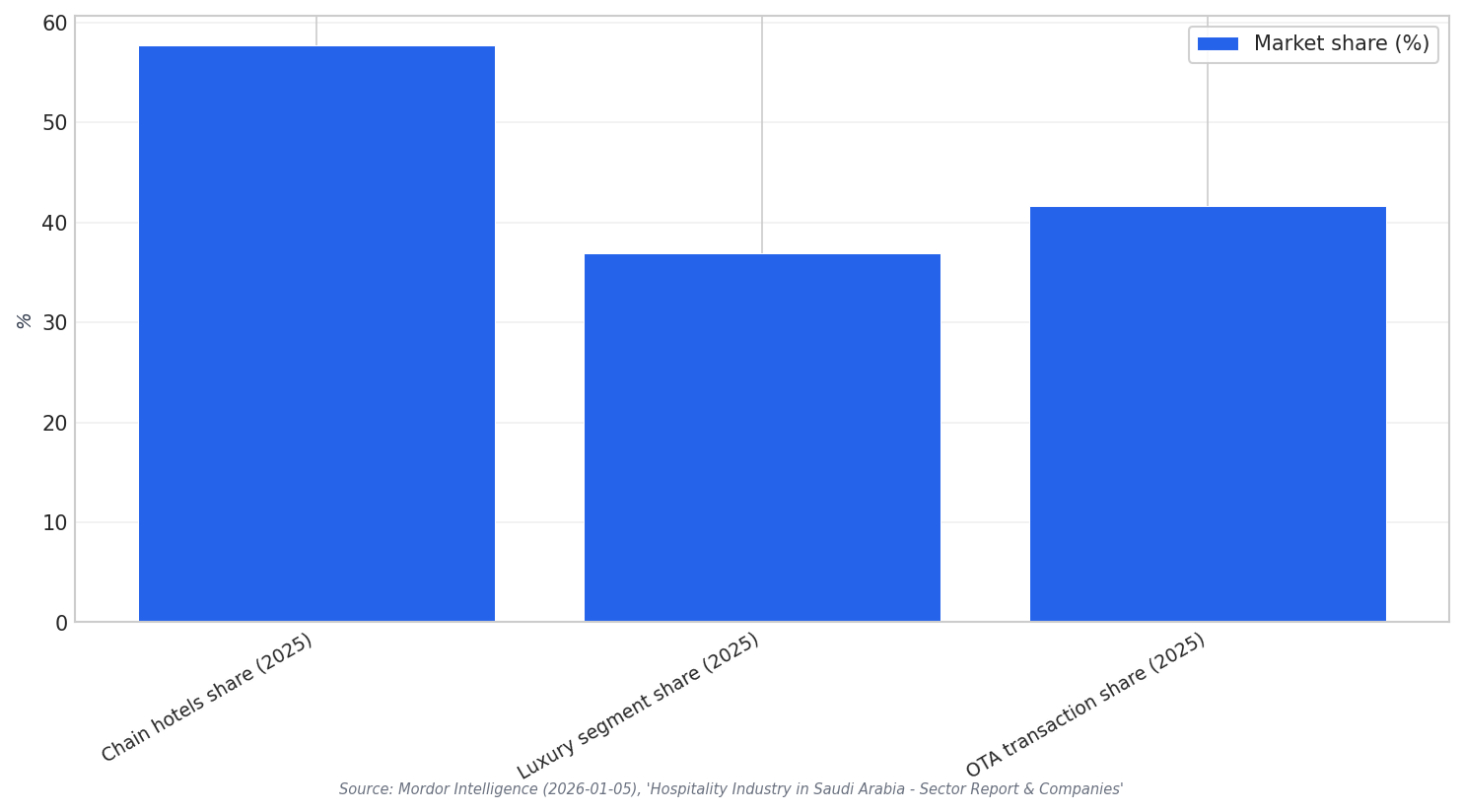

The market backdrop is also expanding. Mordor Intelligence estimates the Saudi Arabia hospitality market size in 2026 at USD 29.02 billion, growing from USD 27.14 billion in 2025, with 2031 projections of USD 40.58 billion. Chain hotels commanded 57.74% of market share in 2025. Luxury led with 36.92% of market size in 2025, while OTAs captured 41.65% of transactions. These figures matter because brand power and distribution capabilities can influence whether an owner prefers an operator-run model or a franchise-led model.

Supply mix can shape the contract choice. Breaking Travel News notes that 75% of upcoming hotel rooms are in the luxury segment, while experts see opportunity in scalable midscale. Mordor Intelligence adds that economy and midscale supply often trails growth in domestic road travel and workforce stays. For investors, a management contract can bring an operator’s systems into a property quickly. A franchise can work when the owner already has operational sophistication, or can appoint an experienced third-party operator.

How Investors Can Compare Management Contracts and Franchises

Management contracts in Saudi Arabia are also evolving. Hospitality Net reports a shift toward lighter management contracts and performance-linked fees. That can align operator compensation with outcomes, but owners still need clarity on performance definitions and remedies. For franchising, the White Sky Hospitality playbook notes that UAE and Saudi Arabia are leading franchise adoption as owners gain operational sophistication. It also describes “manchising,” where owners manage for 3-5 years under a management contract, then convert to a franchise.

Franchising also introduces legal and compliance steps. A Saudi-focused franchise guidance source states the Franchise Disclosure Document (FDD) must be provided at least 14 days before the agreement is signed, as required by the Franchise Law. It adds that lack of compliance may incur fines and can lead to calling off or rejection of contracts. The same source says disputes may be settled through arbitration or mediation, and that the Saudi Center of Commercial Arbitration (SCCA) is one preferred forum. Contract drafting should reflect these realities.

Finally, investors should stress-test the operating model against segment strategy and execution risk. Mordor Intelligence highlights that franchise consistency can be an operational threat in branded economy supply. It also flags common causes of delayed hotel openings in giga projects, including utility readiness, contractor sequencing, and late scope changes. Whether you choose a franchise or a management contract, align brand promises, owner capability, and project readiness before signing.

What is the main decision behind a hotel management contract saudi arabia investors consider?

How big is the near-term hotel room pipeline mentioned in the sources?

What does “manchising” mean in the context of Saudi hotel deals?

What is one franchise compliance point investors should plan for in Saudi Arabia?

What risks can delay openings that investors should consider during contract negotiations?

Talk to us for your needs in:

-

Tourism Infrastructure Planning and Optimization

-

Destination Marketing and Brand Strategy

-

Tourism Workforce Development and Training

-

Sustainable Tourism Solutions

-

Visitor Experience Enhancement and Engagement

-

Tourism Project Feasibility and Strategic Planning

-

Saudi Tourism Benchmarking