Hotel mergers and acquisitions in Saudi Arabia are increasingly framed as a route to speed, scale, and execution certainty, not just ownership change. Industry commentary links the momentum to Vision 2030 initiatives and Expo 2030 expectations, with operators saying they are investing heavily to expand their brand footprint. That backdrop sits within a broader deal market: Saudi Arabia recorded 24 M&A deals worth $689 million in Q1 2026, a 4% annual increase in deal volume, according to Ansarada figures reported by Arab News. In hotels specifically, the narrative is moving away from one-off assets and toward platform logic, where a buyer can build presence faster via a curated set of properties than by developing each asset individually.

Supply mix is shaping where investors look for consolidation and repositioning. One source indicates around 61% of existing hotel inventory is concentrated in luxury and upper-upscale segments, while nearly 78% of new rooms through 2030 are planned at the higher end; another viewpoint states 75% of upcoming rooms are in luxury. That imbalance pushes the M&A thesis toward midscale and economy exposure, especially where demand is durable but ADR assumptions for luxury could be harder to underwrite. Separately, Mordor Intelligence estimates Saudi Arabia’s hospitality market size at USD 29.02 billion in 2026, growing from USD 27.14 billion in 2025, with a projection of USD 40.58 billion by 2031 at a 6.93% CAGR (2026–2031). Those market signals help explain why portfolio plays and conversions are being discussed as a practical way to rebalance segment exposure.

Where Consolidation Is Heading: Portfolios, Conversions, and Clusters

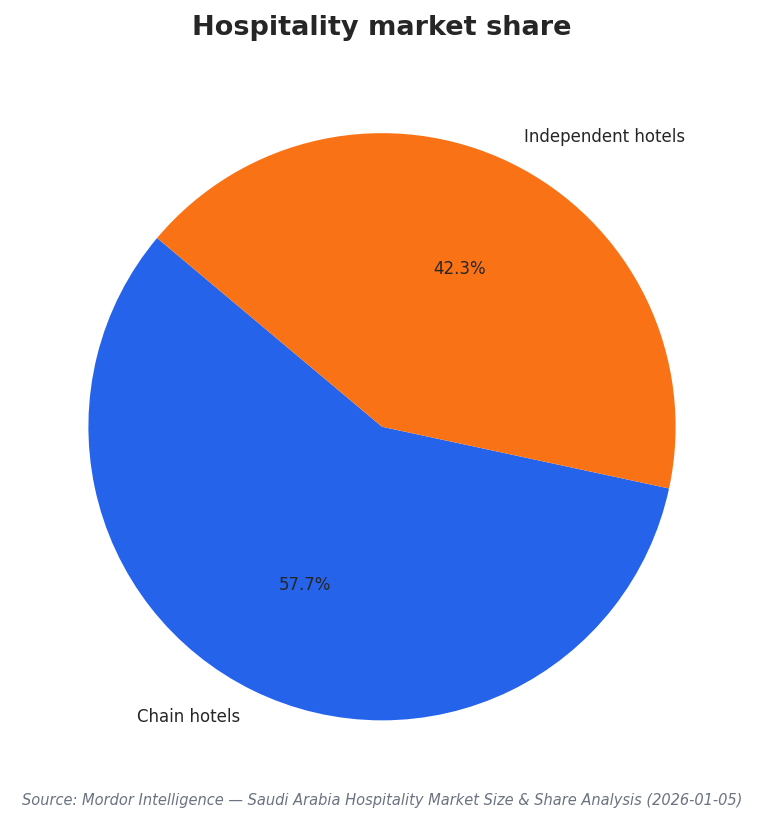

Deal teams are increasingly screening for “asset transformation” opportunities, with conversions and adaptive reuse described as becoming central as owners apply more capital discipline. In practice, that can mean acquiring under-managed assets and repositioning them into scalable brands that can generate repeat business without relying on luxury-rate assumptions. Brand pipelines reinforce the platform approach. Hilton reported surpassing 100 hotels trading and in the pipeline in Saudi Arabia, with 21 operating and 83 in the pipeline, representing a combined investment of USD 8 billion from owners and investors. Meanwhile, Mordor’s segmentation points to continued chain influence: chain hotels held 57.74% market share in 2025, and independent hotels are forecast to trail as chains outpace them with an 11.62% CAGR through 2031.

Investors also have clear geographic and demand-led clustering angles for acquisition targets. Mordor Intelligence notes the Makkah–Jeddah corridor held 26.62% of the Saudi hospitality market size in 2025, while the Red Sea and wider western coast are set to expand at an 18.20% CAGR to 2031. At the same time, tourism volumes are providing a demand floor: total tourist trips (domestic and international) reached 115.9 million in 2024, exceeding the initial target of 100 million, according to a 2025 market analysis. Operators highlight multi-demand mixes, including assets such as Corp Makkah Hotel near Al-Masjid Al-Haram serving pilgrims, tourists, and business visitors, and Corp Hotel Al Khobar serving executives in oil, gas, and petrochemicals—examples that support corridor portfolios spanning religious, corporate, and leisure drivers.

For investors structuring acquisitions, capital market context matters alongside hotel-specific fundamentals. A Saudi real estate M&A analysis reports the asset management industry reached $295 billion in AUM by March 2025, with real estate accounting for 36% of total fund allocations. It also notes that by early 2025, the Saudi REIT market managed SAR 20 billion across 20 funds holding 229 properties, and that Saudi REITs distributed SAR 964.2 million in dividends in 2023. While not hotel-only figures, they indicate active institutional capital and potential consolidation mechanisms that can intersect with hospitality portfolios. Within hotels, the most repeatable target profile emerging from the sources is mid-market scale: portfolios that can be converted, clustered, and integrated into chain operating systems as Saudi Arabia’s tourism and business travel base broadens.

What is driving hotel mergers and acquisitions in Saudi Arabia right now?

Which hotel segments look most under-supplied for M&A repositioning?

What specific figures show Saudi Arabia’s hospitality market growth?

Which locations stand out for clustered hotel portfolio strategies?

How active is the broader Saudi M&A environment that hotel investors operate within?

Talk to us for your needs in:

-

Tourism Infrastructure Planning and Optimization

-

Destination Marketing and Brand Strategy

-

Tourism Workforce Development and Training

-

Sustainable Tourism Solutions

-

Visitor Experience Enhancement and Engagement

-

Tourism Project Feasibility and Strategic Planning

-

Saudi Tourism Benchmarking