Saudi Arabia’s push to scale tourism under Vision 2030 is changing how risk is priced, distributed, and embedded across the visitor journey. Travel cover is moving from an optional add-on to a default purchase step as medical insurance is embedded in the tourist eVisa and stopover programs. A separate 90-day scheme for Umrah and Hajj pilgrims also standardizes coverage across approved providers, making the purchase pathway more consistent for inbound religious travel. In this context, the emerging market for tourism insurance in Saudi Arabia is less about one product and more about an ecosystem that links visas, health benefits, and digital issuance.

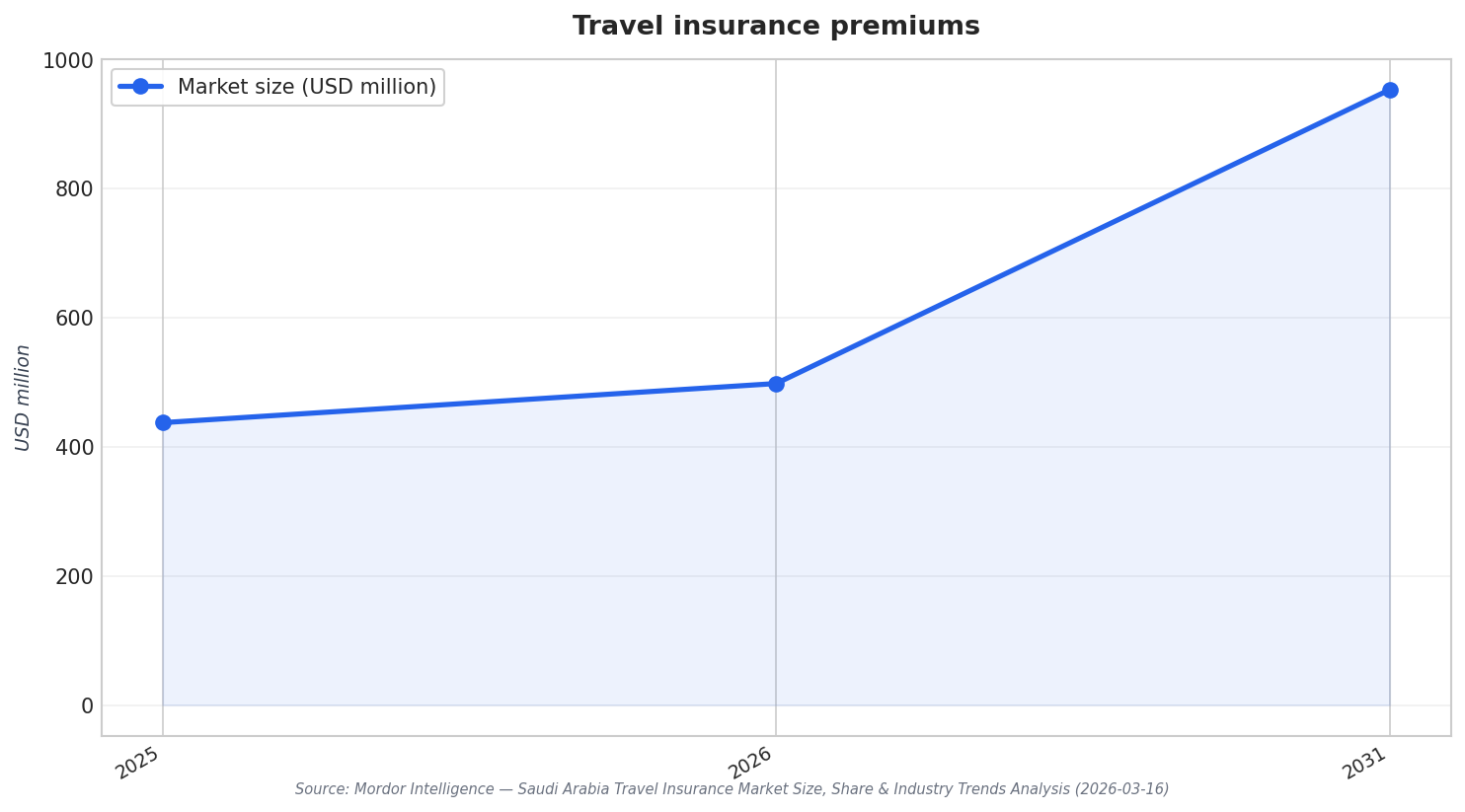

Market forecasts point to sustained momentum. Mordor Intelligence projects Saudi Arabia’s travel insurance premium value to expand from USD 437.41 million in 2025 and USD 498.05 million in 2026 to USD 953.17 million by 2031, a 13.86% CAGR for 2026–2031. The product mix is also clear: single-trip policies accounted for 71.27% of revenue share in 2025, while annual multi-trip offerings are projected to grow at a 10.34% CAGR through 2031. Business travelers held 37.81% of market size in 2025, yet family travelers are forecast to grow fastest at a 10.93% CAGR, suggesting insurers need both corporate-friendly benefits and family-oriented medical and trip protection design.

Where Hospitality Expansion Meets Insurance Demand

The hospitality build-out adds another layer of insurable exposure, from property risk to operational disruption. Mordor Intelligence estimates the Saudi Arabia hospitality market at USD 29.02 billion in 2026, growing from USD 27.14 billion in 2025, with projections reaching USD 40.58 billion by 2031 at a 6.93% CAGR (2026–2031). Chain hotels commanded 57.74% market share in 2025, while independent hotels are forecast to trail as chain operators expand at an 11.62% CAGR through 2031. Luxury led by accommodation class with 36.92% of market size in 2025, and serviced apartments are advancing at a 12.57% CAGR, both of which can require different liability, asset, and guest-related cover structures.

Development scale also matters because giga-project destinations drive concentrated asset values and complex construction and operational risks. The hospitality analysis references Public Investment Fund commitments totalling USD 500 billion to NEOM alone, and complementary projects such as the USD 20 billion Diriyah Gate. NEOM’s Sindalah Island debuted in 2024 with an initial 440 keys, illustrating how new resorts come online with defined capacity that must be protected from day one. In parallel, Mordor’s property and casualty report links engineering lines tailwinds to more than USD 850 billion in giga-projects, supporting a broader shift toward sophisticated commercial cover as Saudi Arabia’s infrastructure and real estate pipeline expands across tourism and hospitality.

Insurers are scaling on two fronts: visitor coverage and commercial risk capacity. Mordor Intelligence projects the Saudi Arabia property and casualty insurance market to grow from USD 9.62 billion in 2025 and USD 11.17 billion in 2026 to USD 23.59 billion by 2031, a 16.12% CAGR for 2026–2031, while noting penetration remains low at 1.5%. A mandatory 30% local reinsurance cession rule enacted in November 2024 redirects premium flows to domestic reinsurers, which can support larger limits for complex projects. Distribution is shifting too: in travel insurance, direct-to-consumer sales via insurers held 31.72% share in 2025, while aggregators are forecast to grow fastest at a 9.51% CAGR, reinforcing the role of digital comparison and instant activation as the default customer expectation.

How is tourism insurance in Saudi Arabia being built into the visa process?

What is the projected growth of Saudi Arabia’s travel insurance market?

Which travel insurance product type leads in Saudi Arabia?

How large is the hospitality market in Saudi Arabia, and why does it matter for insurers?

What policy change is influencing reinsurance capacity for large projects in Saudi Arabia?

Talk to us for your needs in:

-

Tourism Infrastructure Planning and Optimization

-

Destination Marketing and Brand Strategy

-

Tourism Workforce Development and Training

-

Sustainable Tourism Solutions

-

Visitor Experience Enhancement and Engagement

-

Tourism Project Feasibility and Strategic Planning

-

Saudi Tourism Benchmarking