In Saudi Arabia, events are increasingly the demand engine, not just a seasonal spike. One industry view is that the hospitality calendar is now “densely punctuated by events,” and that traditional forecasting can struggle because “the events are the demand.” In that environment, jeddah season matters as part of a broader shift: Jeddah is described as a “gateway city” that is evolving with “strong leisure and cultural appeal.” For operators, this means building plans around peaks and shoulder periods created by programming. For investors, it means underwriting demand that can be driven by multiple generators working together, not one segment alone.

The macro signals behind this shift are already visible in national performance. Saudi Arabia recorded 122 million domestic and international visitors in 2025, a 5% year-over-year increase, and tourism spending rose 6% to nearly SAR 300 billion (about $81 billion). Another source cites 122 to 123 million tourists and the same SAR 300 billion spending figure for 2025. These totals matter to Jeddah-focused stakeholders because the market is described as no longer defined by “one segment or one season,” but by “multiple demand generators working together.” That supports strategies that combine leisure, culture, and event demand around the city.

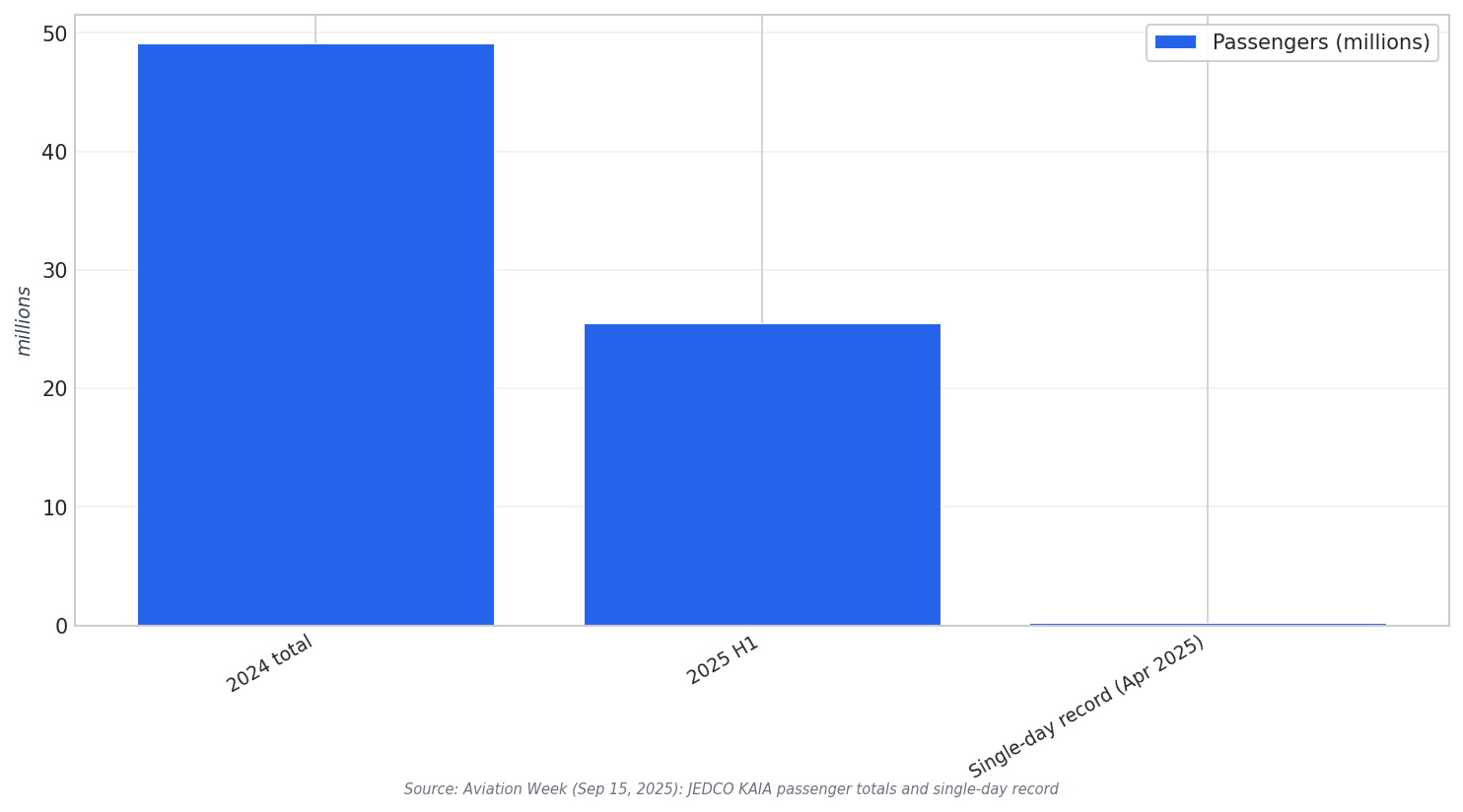

Air access is a practical constraint for any event-led destination, and Jeddah’s airport indicators point to growing capacity utilization. Jeddah Airports Company reported passenger traffic at King Abdulaziz International Airport surpassing 49.1 million in 2024, up 14% year over year. Flight movements increased 11%. Momentum continued into 2025, with 25.5 million passengers in the first half, up 6.8%, and a new single-day record in April of more than 178,000 passengers. For operators planning around jeddah season, these figures reinforce that demand can scale quickly, and that commercial planning should align with airport throughput patterns.

What Operators and Investors Should Do Differently

Product-market fit is a recurring instruction across the sources: the most successful investments “respect local identity while meeting international standards,” and avoid “generic concepts.” That is especially relevant in an event-heavy market like jeddah season, where guest expectations can be shaped by culture-led programming and short booking windows. At the same time, the national hotel pipeline signals a structural gap. Around 61% of existing hotel inventory is still concentrated in luxury and upper-upscale segments, and nearly 78% of new rooms through 2030 are planned at the higher end. Another report similarly notes 78% of upcoming supply concentrated in luxury and upscale tiers. Operators can use this mismatch to position mid-market offerings as resilient, while investors can look at conversions and “asset transformation” as a route to add the right product faster.

Finally, Jeddah’s role can extend beyond standalone leisure. One hotel developer argument is that religious tourism should “blend with the cultural offerings” to extend length of stay and spending, and explicitly says: “You want them to spend time in Jeddah.” This is consistent with the broader thesis that diversification is creating a more resilient investment environment. Government investment “exceeding hundreds of billions of dollars” in infrastructure is cited as a readiness driver that can “enable year-round demand.” For jeddah season stakeholders, the implication is clear: build packages and partnerships that turn event trips into longer itineraries, and build operations that can flex with event-driven volatility while still delivering consistent standards.

What is the strategic relevance of jeddah season for hospitality operators?

What demand signals should investors track around Jeddah?

Is there a hotel segment gap that could shape jeddah season investment?

How can operators reduce seasonality risk in Saudi demand cycles?